In this article, I argue that there exists a dangerous positive feedback loop between land value, embodied in house prices, and the banking system which lies at the heart of modern economies. In response, policies are required to capture more land value for the public good, perhaps through alternative forms of taxation or the creation of public land banks, to help minimise speculative investment in an effort to reduce rising inequality. Different types of banks focused on business lending may also be required. The UK and German economies are compared to shed light on alternative policies.

Andrew Haldane, the Bank of England’s free-thinking Chief Economist, characterised the relationship between modern banks and the state as a ‘doom loop’. Once banks reach a certain size, the state is forced to bail them out if they run into trouble because of the systemic risks they pose to the economy. This relationship creates a perverse incentive for “Too Big To Fail” banks to take more risks than they would otherwise—a key cause of the financial crisis of 2008.

Mr Haldane pointed to the creation of limited liability corporate structures in the late nineteenth century as an important development towards banks growing excessively large. The change in structure capped potential losses for shareholders and encouraged excessive levels of leverage (the ratio of loans to a banks’ equity capital). But another way a bank can limit its losses on a loan is by securing it against property. This can lead to a different, but equally dangerous, doom loop.

If the growth of mortgage lending outpaces the supply of new homes, this will inevitably bid up house prices. As house prices rise, households are forced to take out larger mortgage loans to get on the housing ladder, boosting banks’ profits and capital. This enables them to issue more loans, which further bids up prices until such a point that house prices are many times people’s incomes. In the UK average house prices are now 9 times disposable income, a level similar to that reached before the financial crisis. The process can continue until there is an economic shock (e.g. a rise in interest rates or fall in salaries) and people’s incomes can no longer keep up with debt repayments. Then the whole process goes into reverse – there may be mortgage defaults, falls in house prices, a contraction of bank lending, recession and, potentially, a financial crisis.

Where mainstream economics went wrong

There have always been booms and busts in bank lending. But the analysis in mainstream economics has generally focussed on bank loans issued to businesses, which are part of the ‘business cycle’, and not households. Many economics textbooks describe banks’ main role as the ‘intermediation of household savings for business investment’, or something similar. This definition is not accurate for two reasons. Firstly, banks are not, primarily intermediaries: banks create new money when they make loans—as the Bank of England recently made clear—so intermediation is a misleading term. Second, in advanced economies, the main activity that banks engage in is domestic mortgage lending; not business lending. A recent study of bank credit in 17 countries over the last 120 years by Oscar Jorda, Mauritz Schularick and Alan Taylor found that the share of mortgage loans in banks’ total lending portfolios has roughly doubled over the course of the past century—from about 30 per cent in 1900 to about 60 per cent today.

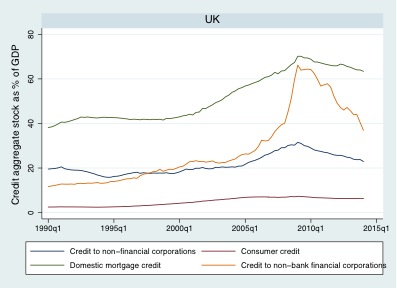

The UK is a prime example. Figure 1 shows that domestic mortgage lending (green line) has expanded from 40 per cent of GDP in 1990 to over 60 per cent now, while lending to non-financial firms has stayed between 20 per cent and 30 per cent of GDP. The UK also saw a huge rise in lending to other non-bank financial corporations (yellow line) but this has contracted considerably since the crisis. In contrast, mortgage lending hardly shrank.

Figure 1: Disaggregated nominal credit stocks as % of GDP in the UK

Thus, in the UK today the majority of new money created for the purchase of existing land and housing—existing assets rather than new, productive assets that enable the economy to expand. And given the limited supply of new homes, the result has been systemic house price inflation well beyond the growth of the economy.

Rising house prices can provide stimulus to the economy. For those lucky enough to own homes, rising prices give us the feeling that we are getting wealthier and encourage us to spend more (the ‘wealth effect’). We can also boost consumption by leveraging the value of our homes by taking out home equity loans or refinancing our mortgages (the ‘collateral’ effect). Given that household consumption contributes around two-thirds of GDP growth in the UK, these are important macroeconomic channels. It is hardly surprising that the first thing the former coalition government did to try and boost the economy post-crisis was to begin subsidising mortgages via the Help-to-Buy equity loan scheme. But ultimately, this macroeconomic approach is not sustainable if debt increases faster than incomes.

UK versus Germany – different banks

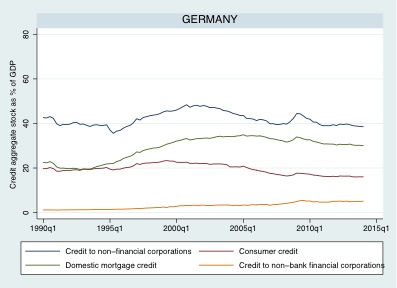

There are alternatives. Although the general pattern in advanced economies has been a shift towards mortgage lending, there are some interesting exceptions to the rule. Figure 2 shows the equivalent breakdown of credit stocks for Germany. Here we see that bank lending to non-financial businesses is significantly higher than mortgage lending at 40 per cent of GDP whilst mortgage lending has only increased to around 30 per cent of GDP.

Figure 2: Disaggregated nominal credit stocks as % of GDP in Germany

Sources: Bank of England and Deutsche Bank data, authors’ calculations

There are two major differences between the UK and Germany that may help to explain these dynamics. Firstly, the countries have very different banking structures. The UK is dominated by four or five very large national or international shareholder owned banks that control around 80 per cent of retail deposits. This is the result of successive waves of deregulation, with banks permitted to engage in mortgage lending in the early 1980s (before then only building societies could do so) and continued relaxation of mortgage lending regulations through the 1990s. This led to the eventual swallowing up of much of the mutual sector via mergers and acquisitions.

The UK has a strong ‘transaction’ banking culture. This is characterised by a preference for short-term business loans, centralised credit-scoring techniques to make decisions, a need for high quarterly returns on equity and a strong preference for collateral. Crucially, UK banks prefer lending against existing assets—In particular property or land—which they can repossess in case of default. In contrast, in Germany there is a much stronger culture of ‘relationship banking’. Two-thirds of bank deposits are controlled by either cooperative or public savings banks, most of which are owned by regional or local stakeholders. These ‘stakeholder banks’ are focused on business lending and do not have such stringent collateral requirements. They tend to devolve decision making to branches and rely on building up strong relationships and understanding of businesses as a way to de-risk their lending.

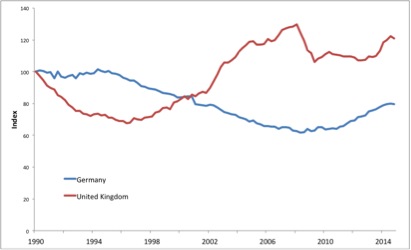

The second key difference is that Germany has a very different land economy. They have less stringent planning laws and a relatively elastic supply of land. As a result, Germany has a diverse construction industry, including private and cooperative developers and a strong self-build industry. In addition, only a half of Germans own their own homes with the rest enjoying a well-regulated private rental sector offering much better quality and security than the UK. The result is that average house prices have changed little in Germany over the last few decades. In fact, as shown in Figure 3, the house price to income ratio actually dropped in Germany during the 2000s, in contrast to a huge and unsustainable expansion in the UK.

Figure 3: House price to income ratio, Germany and the UK, 1990-2014 (1990=100)

Source: OECD

In the UK, we have a tightly controlled planning system and a construction industry dominated by large private shareholder firms (not dissimilar to our banking system). Public sector home building collapsed in the mid-1980s. Even now, when private developers get hold of land, there is no guarantee they will build on it since the rate of land appreciation is such that it may make more sense to simply to ‘bank’ it or trade it.

The strong culture of home ownership in the UK is also driven by the potential for speculative gain. As our pensions and social security have been reduced by successive governments and median wages have stagnated, homes have become seen as a way of investing in our own future economic security. Government policy has encouraged this shift towards ‘asset-based welfare’.

All these factors—a combination of financial deregulation, ill thought out planning and housing policy and changes in welfare—have resulted in land and housing in the UK becoming ‘financialised’. ‘Getting on the housing ladder’ may sound like an innocuous phrase, but it in fact refers to accessing the most desirable financial asset, capable of increasing our paper wealth many times more than moving job or investing in the stock market or government bonds.

The result is a seemingly never-ending housing bubble. The current bubble is being maintained by government policy, just like the last one. The latest intervention is a huge expansion of George Osborne’s ‘Help-to-Buy’ scheme. The government is going to offer equity loans to first-time buyers on a massive scale as well as investing in new home building by subsidising private developers.

New build homes are to be welcomed but there is little evidence that private sector homebuilders are capable of building on the scale required. It also seems likely that guaranteeing mortgages on this scale will worsen our already precarious household debt to income ratio. Research by Shelter found the previous Help-to-Buy scheme raised average house prices by over £8,250. One wonders what the Bank of England, which recently sounded the alarm about the Buy-to-Let market overheating, makes of such a scheme.

Solutions

To break the land-economy-finance doom-loop, multiple interventions are required to both our financial system and our land economy. We need to refocus our banks and the wider economy on productive investment, including the building of homes, and away from lending against existing assets. Breaking up one of our part-nationalised mega-banks in to a network of regional banks owned by local stakeholders and focused on local business relationship lending seems like an obvious option.

Unlike other commodities, land is not subject to the standard rules of mainstream economics. It is finite and more of it cannot simply be ‘produced’ when demand increases. As a result, access to, control over and ownership of land, particularly in economically desirable areas, enables individuals and companies to earn vast windfall profits.

There is thus a strong case for public interventions in the way land is taxed, controlled and used. The speculative profits arising from owning desirable land could be taxed or captured by local or national governments—or perhaps communities—by virtue of being the owners of the land themselves. In many East Asian countries, such as South Korea, Hong Kong and Singapore, the majority of land is controlled by state corporations—public ‘land banks’. In the US and Canada, there are similar schemes at the state or local government levels.

These may seem like radical structural interventions to the shape of our economy But the alternative is worsening inequality, rising prices and rents and, eventually, another crisis as the bubble bursts yet again.

Josh Ryan-Collins is the Associate Director of Economy and Finance at the New Economics Foundation.

This article is part of a blog series building on three seminars co-hosted by Oxford’s Department of Politics and International Relations, the New Economics Foundation and Positive Money.

This blog series aims to inform public and policy debate on the role of public assets in our political economy. The series and related seminars were supported by the University of Oxford’s ESRC Impact Acceleration Account.

Comments

{kind=link}

{kind=link}

1 Comment